Banks' Endeavour to Buyout NBFCs' Loan Book is Synergetic

By MYBRANDBOOK

India Ratings and Research (Ind-Ra) believes that the steps taken by Reserve Bank of India (RBI) to support systemic liquidity and State Bank of India (SBI; IND AAA/Stable) to offer balance sheet liquidity for non-banking financial companies (NBFCs) would help alleviate some of the ongoing tightness in the financial system. These measures however are likely to bring about a temporary effect. For long-term sustainability, restoration of normalcy in the credit market especially for NBFCs is critical. Additionally, development of alternative sources of financing such as an active securitisation market would be beneficial.

Actions to Complement System and Balance-sheet Liquidity:The RBI has recently infused INR320 billion of durable liquidity into the system and another INR240 billion is likely to come in the month of October 2018 through open market operations. In addition, to tide over frictional liquidity mismatches, banks are now permitted to reckon SLR securities held by them up to another 2% of their net demand and time liabilities, under the facility to avail liquidity for liquidity coverage ratio within the mandatory SLR requirement. Ind-Ra believes this will help in stabilising the systemic liquidity, especially in light of possible draining of liquidity in the upcoming festive session. SBI has announced an additional INR300 billion asset buyout from NBFCs, which would help them tide over the ongoing challenges.

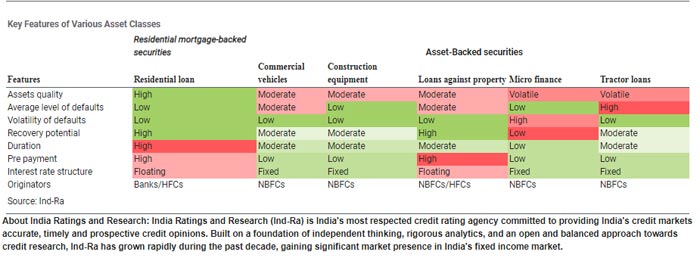

Potential Source of Liquidity for NBFCs: Ind-Ra has analysed the top eight housing finance companies (HFCs; excluding HDFC Ltd and LIC Housing Finance Limited) and the top 10 non-infrastructure NBFCs. Of the total, 16 entities (are among the largest NBFCs) have about INR5 trillion exposures to asset classes that are preferred (most common are microfinance, commercial vehicles, housing loans etc) for assignment or securitisation. According to the announcement by SBI, it is expected to purchase over INR450 billion (about three times of normal buyouts) of assets from NBFCs over FY19 to create additional source of liquidity for non-banks. Some of the well-capitalised banks, many of which are approaching their sectoral cap on NBFCs, may also expand their buyouts of assets as an alternative to expand funding to non-banks.

Banks can Cherry Pick Assets: As opposed to the asset classes which are typically securitised or assigned, originating granular housing loans, commercial vehicle loans and other such asset classes involves significant operating costs and banks may not have the adequate network to originate them or assess credit quality on a large scale. In the current environment, banks could cherry pick assets from NBFCs and price them well instead of originating them, thus avoiding scope for early delinquencies. This proposition is likely to result in better RoAs for banks on both priority sector lending qualifying assets and others that are securitised / assigned.

Ind-Ra also expects other banks (including private banks) with adequate capital buffers to use a similar strategy to cherry pick assets from NBFCs. Additionally, exposure to these assets does not amount to exposure to NBFCs’ balance sheet and hence this route partly addresses the perceived risk aversion. NBFCs will see some relief on the perception of inadequate liquidity over 3QFY19 and the securitisation push would be conducive for matching assets with liabilities. This is also an opportunity for NBFCs to reduce dependence on short-term funding, as they take some assets off the balance sheet.

Decelerating Credit Flows from Non-Banks: The recent data from mutual funds suggest that there has been a considerable drop in assets under management under liquidity fund in September (part of which is seasonal), after a sudden rise in August. Asset management companies have been the largest subscribers of money market instruments and have been instrumental for the surge in NBFCs’ business in the last few years. Overall, incremental inflows into debt funds have decelerated and therefore supply funding could be restricted. This scenario could not only impinge NBFCs’ growth but also pose refinancing challenges, especially for the newer and weaker NBFCs. In these circumstances, monetisation of assets through securitisation to address short-term financing requirements could be beneficial. The current situation also strengthens the necessity of developing a securitisation market for stakeholders to ensure a sustainable funding option along with traditional sources.

Nazara and ONDC set to transform in-game monetization with ‘

Nazara Technologies has teamed up with the Open Network for Digital Comme...

Jio Platforms and NICSI to offer cloud services to government

In a collaborative initiative, the National Informatics Centre Services In...

BSNL awards ₹5,000 Cr Project to RVNL-Led Consortium

A syndicate led by Rail Vikas Nigam Limited (abbreviated as RVNL), along wi...

Pinterest tracks users without consent, alleges complaint

A recent complaint alleges that Pinterest, the popular image-sharing platf...

Netflix adds 'Moments' feature for saving, sharing scenes from

Netflix has introduced a new “Moments” feature on its mobile app, whic

Jacqueline Fernandez come together with YouTuber Mr. Beast for

Jacqueline Fernandez has partnered with American YouTuber Mr. Beast to b

Visa elevates Rishi Chhabra as new Country Manager for India

Rishi holds a Master’s in Industrial Engineering from The Ohio State Univ

Genesys welcomes Albert Nel as Senior VP and Regional Sales Le

Genesys continues to deepen its investment in the APAC region. Earlier this

AMD Pensando driving innovation in the DPU architecture space

AMD Pensando stands out in the DPU (Data Processing Unit) market with its u

Bolstering its commitment to help build a truly self-reliant B

CP PLUS is dedicated to spreading a sense of security to every corner of In

SonicWall Launches TZ80: A Powerful Solution for Remote Office

SonicWall announced today the launch of the TZ80, a groundbreaking securit

Gigabyte X3D Turbo: A Gaming Revolution

GIGABYTE X3D Turbo Mode is a cutting-edge feature that unifies cores distr

FRESHWORKS TECHNOLOGIES PVT. LTD.

SAFE SECURITY SERVICES PVT. LTD.

TATA CONSULTANCY SERVICES

HP INDIA SALES PVT. LTD.

ICONS OF INDIA : SANJAY NAYAR

Sanjay Nayar is a senior finance professional in the Indian private in...

ICONS OF INDIA : SOM SATSANGI

With more than three decades in the IT Sector, Som is responsible for ...

Icons Of India : Anil Kumar Lahoti

Anil Kumar Lahoti, Chairman, Telecom Regulatory Authority of India (TR...

BSE - Bombay Stock Exchange

The Bombay Stock Exchange (BSE) is one of India’s largest and oldest...

GeM - Government e Marketplace

GeM is to facilitate the procurement of goods and services by various ...

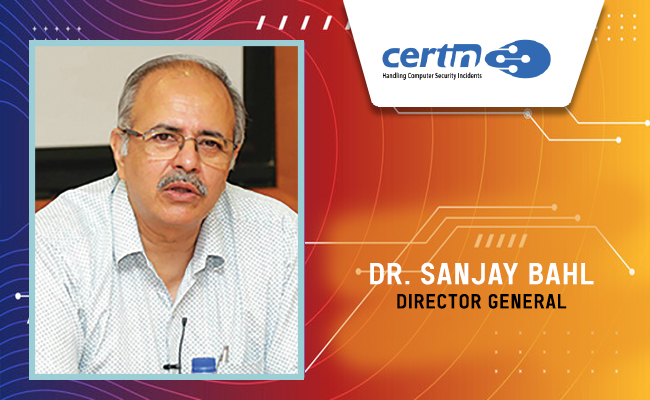

CERT-IN - Indian Computer Emergency Response Team

CERT-In is a national nodal agency for responding to computer security...

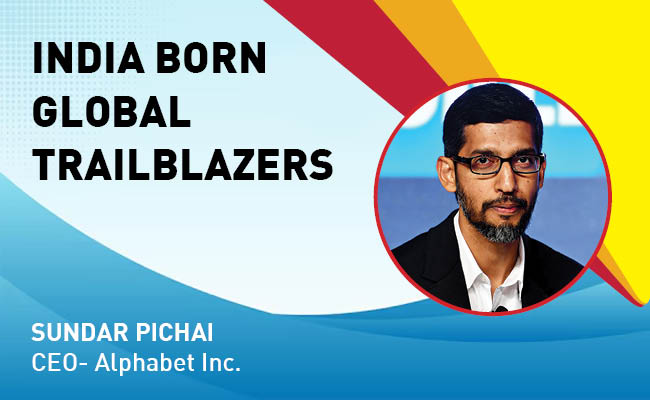

Indian Tech Talent Excelling The Tech World - Sundar Pichai, CEO- Alphabet Inc.

Sundar Pichai, the CEO of Google and its parent company Alphabet Inc.,...

Indian Tech Talent Excelling The Tech World - ANJALI SUD, CEO – Tubi

Anjali Sud, the former CEO of Vimeo, now leads Tubi, Fox Corporation�...

Indian Tech Talent Excelling The Tech World - Rajiv Ramaswami, President & CEO, Nutanix Technologies

Rajiv Ramaswami, President and CEO of Nutanix, brings over 30 years of...