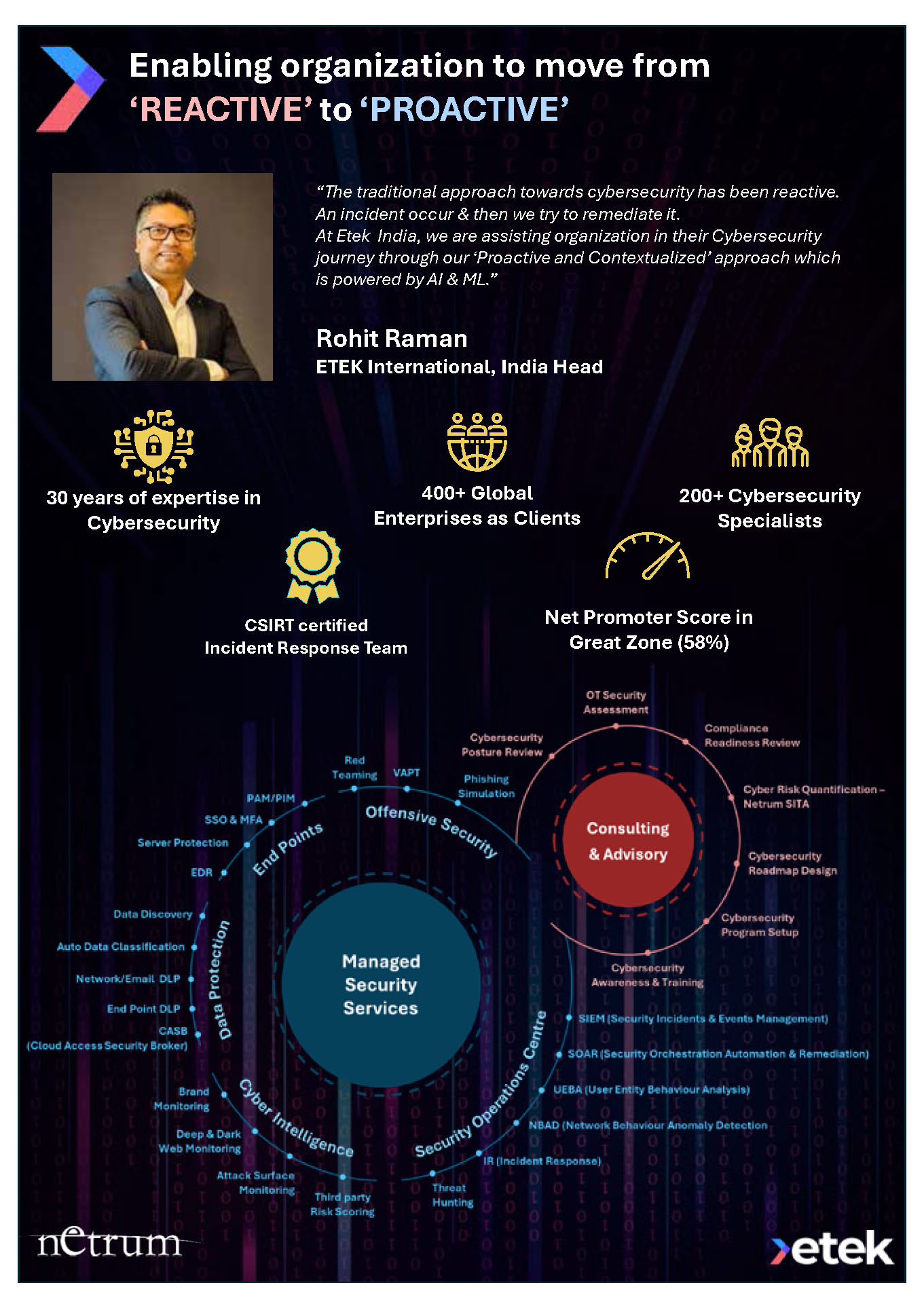

Indian IT Services Industry has a stable outlook - ICRA

By MYBRANDBOOK

Expected CAGR for FY2018-2021e to be around 9-12% IT players compared to CAGR of 17.1% over FY2013-2017

ICRA has a stable outlook on Indian IT Services industry. The credit profile of Indian IT Services companies remains stable underpinned by its ability to sustain free cash flows despite pressure on revenue growth and margins. With aggregate operating margins of ICRA sample set at 22.5% for FY2018 coupled with moderate capex (organic as well as inorganic) and working capital requirements, the free cash flows have remained robust historically. Despite pressures on growth and margins over the medium term, these factors are unlikely to impact the free cash flow generation ability of Indian IT Services companies though there could be moderation in the quantum of such cash flows. The credit profile is also supported by net cash position with significant liquidity in the form of surplus investments generated out of past cash flows. Our sample set (13 leading Indian companies) reported surplus liquidity (net of debt) of approximately Rs. 1,600 billion March 2018 despite healthy dividend pay-out of approximately 30% (Rs. 206 billion) in addition to share buybacks (Rs. 73 billion).

ICRA expects most large IT services companies to maintain high dividend pay outs and share buybacks, as there are limited avenues for fund deployment. The investment requirements (organic and inorganic) for Indian IT Services in the past have been moderate relative to internal cash flow generation. Majority of the acquisitions done by Indian IT Services players have been to acquire competencies rather than achieve scale and size.

The growth of Indian IT Services companies will be impacted by lower deal sizes in digital technologies, cloud adoption and high competitive intensity from local as well as international players. While companies have increased spending on digital technologies and awarding new contracts, the overall IT budgets have moderated leading to lower incremental spends. Indian IT Services companies are re-orienting their business models focusing more on high end services such as IT consulting & emerging technologies (digital) and have made considerable progress so far, though it currently lags international peers. ICRA expects FY2018-2021e CAGR to be around 9-12% for the Indian IT Services companies compared to CAGR of 17.1% experienced over the FY2013-2017 period.

Margins will be supported by factors such as ability to modify cost structure with rational and variable salaries couples with gradual reduction of high cost resources. Besides deployment of operating levers such as higher share of fixed price contracts, lesser idle resources & automation benefits will also help manage costs. However, these factors will provide limited cushion leading to overall decline in operating margins from 22.1% in FY2018 to 20.8% in FY2021e for ICRA sample companies (13 leading companies).

Nazara and ONDC set to transform in-game monetization with ‘

Nazara Technologies has teamed up with the Open Network for Digital Comme...

Jio Platforms and NICSI to offer cloud services to government

In a collaborative initiative, the National Informatics Centre Services In...

BSNL awards ₹5,000 Cr Project to RVNL-Led Consortium

A syndicate led by Rail Vikas Nigam Limited (abbreviated as RVNL), along wi...

Pinterest tracks users without consent, alleges complaint

A recent complaint alleges that Pinterest, the popular image-sharing platf...

Netflix adds 'Moments' feature for saving, sharing scenes from

Netflix has introduced a new “Moments” feature on its mobile app, whic

Jacqueline Fernandez come together with YouTuber Mr. Beast for

Jacqueline Fernandez has partnered with American YouTuber Mr. Beast to b

Visa elevates Rishi Chhabra as new Country Manager for India

Rishi holds a Master’s in Industrial Engineering from The Ohio State Univ

Genesys welcomes Albert Nel as Senior VP and Regional Sales Le

Genesys continues to deepen its investment in the APAC region. Earlier this

Delivering Critical Business Communication Solutions to Enterp

Arya Omnitalk and Syntel’s comprehensive suite of solutions and more than

Autodesk continually pushing the boundaries in the Design and

Autodesk’s vision is of a better world designed and made for all. It inte

SonicWall Launches TZ80: A Powerful Solution for Remote Office

SonicWall announced today the launch of the TZ80, a groundbreaking securit

Gigabyte X3D Turbo: A Gaming Revolution

GIGABYTE X3D Turbo Mode is a cutting-edge feature that unifies cores distr

ALPHAMAX TECHNOLOGIES PVT. LTD.

CENTRE FOR DEVELOPMENT OF TELEMATICS (C-DOT)

VEHERE INTERACTIVE PVT. LTD.

LUMINOUS POWER TECHNOLOGIES PVT. LTD.

Icons Of India : MUKESH D. AMBANI

Mukesh Dhirubhai Ambani is an Indian businessman and the chairman and ...

Icons Of India : RAJENDRA SINGH PAWAR

Rajendra Singh Pawar is the Executive Chairman and Co-Founder of NIIT ...

Icons Of India : PRATIVA MOHAPATRA

Prativa is a transformational leader with an incredible breadth of exp...

LIC - Life Insurance Corporation of India

LIC is the largest state-owned life insurance company in India...

GeM - Government e Marketplace

GeM is to facilitate the procurement of goods and services by various ...

CSC - Common Service Centres

CSC initiative in India is a strategic cornerstone of the Digital Indi...

Indian Tech Talent Excelling The Tech World - REVATHI ADVAITHI, CEO- Flex

Revathi Advaithi, the CEO of Flex, is a dynamic leader driving growth ...

Indian Tech Talent Excelling The Tech World - ARVIND KRISHNA, CEO – IBM

Arvind Krishna, an Indian-American business executive, serves as the C...

Indian Tech Talent Excelling The Tech World - NEAL MOHAN, CEO - Youtube

Neal Mohan, the CEO of YouTube, has a bold vision for the platform’s...